This week’s letter comes to you from frigid Ontario, where Joe, Jr. is attending a small meeting of fellow business owners. We find it helpful to share ideas and learn from people in other fields, especially how they see trends in important areas like artificial intelligence. And the weather is an adventure for your Floridian financial advisor.

-------------------------------------------------------------------------------------------------------------------------------------------

We remain convinced that long-term economic success relies on healthy demographic trends, especially birthrates. This article addresses a gap in the way fertility rates are often discussed, accounting for how women are having children later in life. It shows that the U.S. is in a good place relative to its peers.

Do AI-driven Large Language Models (LLMs) increase productivity? This paper argues that they do. We would agree.

Utah is allowing a pilot AI system to handle routine prescription renewals. The American Medical Association has some reservations. It will be an interesting test.

Do GLP-1 reduce other expenses, justifying their cost? Maybe, but not in the short-term, as this paper argues.

You may be listening to AI-generated music without knowing it. An AI artist has 3 songs in Spotify’s Top 50.

-------------------------------------------------------------------------------------------------------------------------------------------

Q: I’m interested in a new book by Aaron Ross Sorkin, 1929- are we in danger of a depression?

A: It is tempting to look at history and think about whether the next big crisis or recession will look like the last one, or the one before. With generally rosy forecasts for the market this year, it is reasonable to wonder what could go wrong.

We don’t think that a 1929 (or 2008) scenario is likely. The spending and enthusiasm for AI may well be overblown, but a correction in that sector would not have the pervasive impact of the financial/housing crisis.

So what does this year hold? We don’t know, and the beginning of the year has been full of the kind of policy and geopolitical noise that has become more common. Last week, Chris Fasciano wrote here:

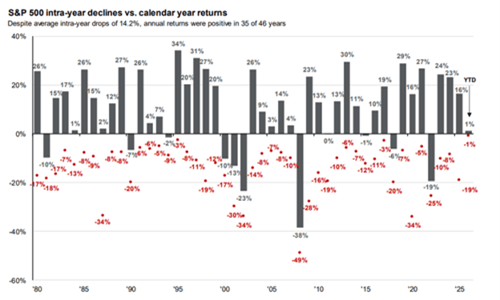

With these headlines swirling, it wouldn’t have been surprising if markets started the year lower. But as of the Friday (1/14/2026) close, they haven’t. Although that could certainly change. Most years, there is a sell-off of some magnitude. It is usually at least a double-digit percentage negative decline. The early 2000s saw three straight years of negative returns. Over the past 23 years since then, only four of those years saw a negative return for the S&P 500; in two of those years, the returns were single digits (1 percent and 6 percent) (see chart below).

![]()

It would be surprising if we didn’t see a similar correction at some point in 2026. Last year, we experienced a 19 percent decline early in the year; ultimately, the market rallied to return just under 16 percent. The lesson of last year was that policy can change and headlines will dissipate. Through the end of last week, investors seemed to be counting on that happening again and the impact on the U.S. economy being minimal.

We don’t know what the year will bring, but the rules of prudent investing haven’t changed.